Are you pricing your garments based on rough factory quotes or competitor prices, then realizing too late that your margin disappears once trims, wastage, printing, packaging, freight, and duties are added? Accurate garment costing is one of the most important skills in apparel manufacturing. It affects your pricing strategy, profit margin, cash flow, MOQ decisions, and even which fabrics and factories you can realistically work with. When costing is incomplete, brands quietly lose money through hidden charges, rework, wastage, rushed shipments, and last-minute changes. When costing is accurate, you can negotiate confidently, plan production timelines, set realistic retail pricing, and scale without constant surprises.

This guide gives you a practical, manufacturer-ready method to calculate garment production cost accurately, from fabric consumption and trims to labor, overhead, processing, packaging, FOB, landed cost, and margin math.

What Garment Production Cost Really Means

Garment production cost is the total cost to produce one finished unit based on exact materials, construction, and processes. Many brands assume the factory quote is the full cost. In reality, accurate costing separates production cost from export cost and landed cost, then connects that to your selling price and target margin, ensuring a comprehensive understanding of actual costs.

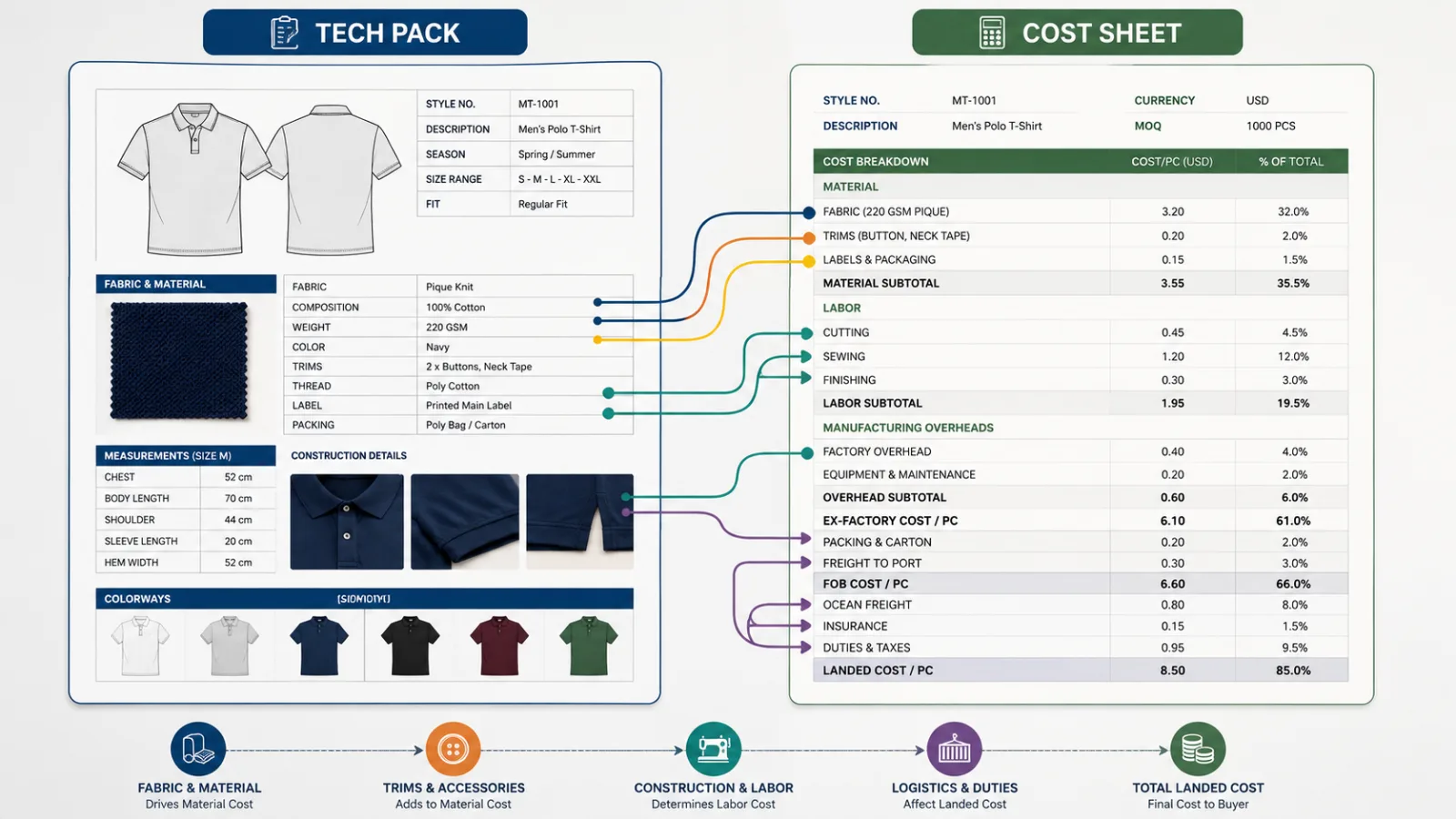

A clean way to think about costing is in three layers. Ex-factory cost is what it costs to produce the garment at the factory gate, including fabric, trims, cut and sew, printing or embroidery, washing, finishing, packaging, and factory overhead. FOB cost includes ex-factory plus export handling and port delivery costs. Landed cost includes FOB plus freight, insurance, duties, and destination handling. When you know all three, you can price your garments with confidence.

Garment Costing Methods and Techniques

In fashion manufacturing, understanding garment costing and pricing begins with knowing how to calculate the cost of producing and the cost of making a style from initial garment designs through sampling and full-scale runs; the costing process must capture materials and labor, sampling expenses, and both direct and indirect costs so teams can calculate the true cost and the cost of the garment. Effective cost control and cost reduction strategies help streamline production and lower overhead costs and other operating expenses that drive costs higher.

Different approach to costing methods — including direct costing, variable costing, absorption costing, job costing / job order costing, and target costing — inform how to allocate costing data across the number of units in mass production or bespoke runs, enabling calculation of total cost of producing, total cost per hour, and better financial reporting. Anyone who needs to know about garment costing should know about garment costing fundamentals to accurately compute the cost of production and make profitable decisions.

Why Accurate Costing Matters for Apparel Brands

Costing is not only finance. It is a product strategy, particularly when incorporating a detailed bill of materials to outline all necessary components. Accurate costing helps you choose the right fabric, construction, and trims for your target price point. It also helps you avoid common margin killers like label MOQ problems, printing setup fees, high wastage, inaccurate fabric consumption, and freight surprises.

Accurate costing protects your brand in another way too. Many quality issues begin as costing issues. If a brand pushes pricing too low, the manufacturer may substitute trims, reduce stitch quality, or use a different fabric finish. When your cost sheet is detailed and transparent, you can reduce cost smartly without damaging product quality.

Global Apparel Production Cost Trends

The global apparel industry operates at massive scale. Industry research shows the number of garments produced annually has exceeded 100 billion since 2014, which is one reason cost efficiency is a constant priority for both brands and manufacturers. From a production-cost perspective, fabric is usually the biggest cost driver. In basic-styled garments, fabric can account for around 60–70% of total garment cost, which is why accurate fabric consumption, marker efficiency, and wastage control directly impact profitability and the overall material cost.

Cost pressure is also rising because of waste and logistics realities. The world produces about 92 million tonnes of textile waste every year, reinforcing why better planning, better forecasting, and accurate costing matter for sustainability and margin protection. On the logistics side, global shipping disruptions have driven freight cost volatility, and higher freight rates can quickly increase landed cost for brands importing from major manufacturing hubs.

Garment Cost Breakdown Example

Understanding how garment production costs are distributed can help apparel brands make better pricing and sourcing decisions. While the exact percentages vary depending on garment type, fabric quality, and production complexity, most apparel products follow a similar cost structure. Fabric typically represents the largest portion of garment production cost, followed by labor and trims. Additional costs such as printing, packaging, and quality control also contribute to the final cost of a garment. The table below shows a general example of how production costs may be distributed in apparel manufacturing.

Cost Component: The estimated share of Total Cost, including material cost and labor, is crucial for effective budgeting.

These percentages may vary depending on the garment category. For example, fashion garments with complex trims and embroidery may have higher embellishment costs, while basic apparel products often allocate a larger share of cost to fabric. For apparel brands, understanding this cost distribution helps improve production planning, optimize material sourcing, and maintain healthy profit margins throughout the supply chain, particularly by analyzing the true cost of raw materials.

Main Factors that Affect Garment Costing

In fashion manufacturing, the main factors that affect garment costing include materials, labor, overhead, and efficiency when producing a garment. Understanding garment costing and pricing means you must know about garment costing methods like direct costing, absorption costing, and variable costing, so you can calculate the true cost and the cost of the garment. An effective approach to costing uses costing data from both direct and indirect costs to determine the total cost of producing a style and the total cost per hour on the line.

Manufacturers apply techniques such as job costing or job order costing, and target costing to set prices and achieve cost control. Accurately calculating the cost of materials, trims, and labor for specific garment designs lets teams forecast the cost of production and spot opportunities for cost reduction.

Overall, a thorough analysis of the components of apparel costing and ongoing measurement of processes ensures that costing reveals profitability and supports competitive pricing.

Why Is Garment Costing Important?

In apparel production, resource planning and accurate estimating are essential because costing ensures you account for total production costs and understand the garment’s cost before committing to orders. it’s important to know how each raw material, labor hour, and overhead item will affect the bottom line and how a manufacturing agreement will influence timelines and expenses.

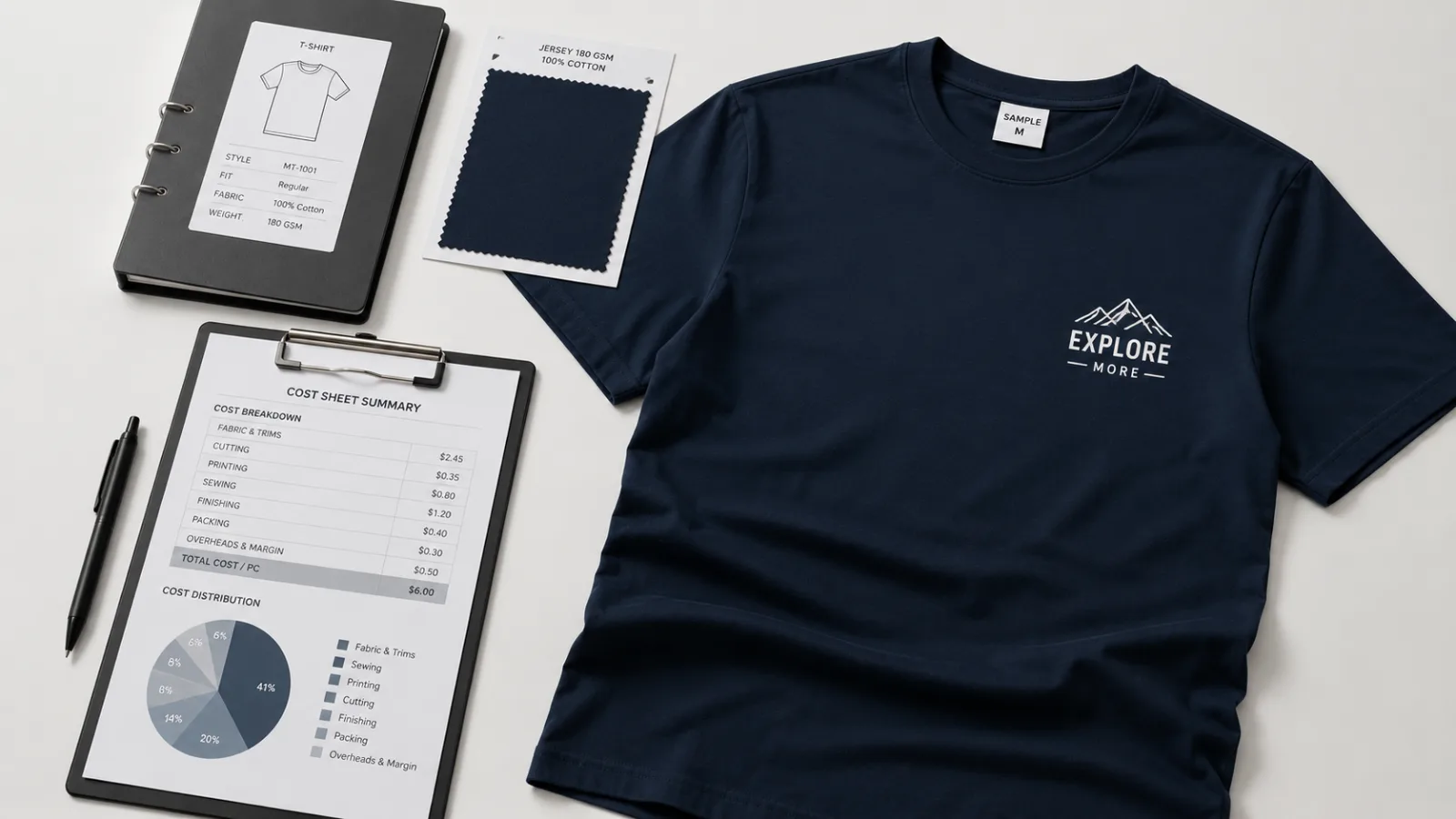

Good pricing and profitability depend on detailed analysis: to set the right price you must quantify inputs precisely, since costing means breaking down every element into measurable figures. A clear cost sheet is a document used to calculate what an order is going to cost, listing fabrics, trims, labor, and margins. Accurate costing plays a significant role in contract negotiation, risk management, and ensuring sustainable margins throughout the product lifecycle.

The Costing Framework You Should Use

A reliable garment costing framework looks like this:

Ex-factory cost per unit = Fabric + Trims + Cut and Sew + Processing (print, embroidery, wash) + Packaging + Wastage + Overhead + Quality and testing allowance

FOB cost per unit = Ex-factory cost + Export forwarding, documentation, port delivery costs (allocated per unit)

Landed cost per unit = FOB cost + Freight + Insurance + Duties and taxes + Destination handling (allocated per unit)

This framework works because it forces you to account for every cost driver that affects real profitability. It also makes factory quotes comparable, because you can see what is included and what is missing.

Costing Inputs You Must Confirm Before Calculating

Costing becomes inaccurate when you calculate based on unclear product specs. Before costing, confirm your key inputs from the tech pack and sampling plan. These inputs control consumption, wastage, line efficiency, and trim requirements.

You should confirm garment category, fabric type, GSM and width, number of colors, size range, stitching complexity, trims list, branding method, packaging standard, order quantity, and target delivery timeline. A small change like adding an embroidery patch or switching fabric GSM can change unit cost more than many brands expect. Treat these inputs like a costing checklist. If something is unclear, your costing is only an estimate and should be labeled as such until the sample stage confirms it.

Image Prompt: Tech pack cover page beside fabric roll labels showing GSM and width, trims list visible on a clipboard, realistic desk photo, 16:9

Fabric Cost Calculation That Matches Real Production

Fabric is usually the biggest cost driver, especially for heavyweight knits, premium fleece, and woven garments. Accurate fabric costing requires two numbers: the fabric price and the fabric consumption per garment. The key is not only price per kg or per yard. The key is consumption plus realistic wastage.

A practical formula is:

Fabric cost per unit = Fabric consumption per unit × Fabric price per unit measure × (1 + fabric wastage percent)

Consumption is ideally based on marker efficiency data from the factory. If you do not have marker data yet, you can estimate conservatively using pattern size and fabric width, then refine after sampling to align with garment costing methods.

For knits, many factories convert consumption into kg per piece using GSM and pattern area. For wovens, consumption is often measured in meters or yards based on marker length. In both cases, your best results come from requesting estimated consumption from the factory during sampling.

Fabric Wastage: The Hidden Cost You Cannot Ignore

Wastage is not optional. It is the real cost from end loss, market inefficiency, fabric defects, shade variation, cutting loss, and handling damage. Brands often apply random wastage numbers, but wastage should be connected to garment type and fabric behavior.

Simple knits often have lower wastage than complex wovens. Stripes, checks, or pattern matching requirements reduce marker efficiency and increase wastage. Small pieces, many panels, or special placement needs also increase wastage. A realistic approach is to include wastage as a line item that you refine over time. For new styles, use conservative wastage assumptions and reduce them only after actual production data confirms lower loss.

Trims Cost Using a Complete BOM

Trims include everything besides the main fabric: labels, threads, buttons, zippers, drawcords, elastics, hangtags, patches, barcodes, size stickers, polybags, and cartons. Trims are where many brands lose money quietly because trim MOQs and setup costs are ignored.

A simple trim formula is:

Trim cost per unit = Sum of (quantity per garment × unit price of each trim) + trim wastage or MOQ allocation MOQ allocation matters. If a hangtag supplier requires 5000 tags and you only need 1000, the extra cost still exists. You either carry inventory or allocate that cost across your first run. Seeing it clearly in the cost sheet helps you make better decisions, like standardizing hangtags across multiple styles.

Cut and Sew Cost: Understanding Labor Beyond Sewing

Factories often quote a CMT price (cut, make, trim) or a sewing price per piece, but labor cost depends heavily on garment complexity and production efficiency. A basic t-shirt is quick to produce. A lined jacket requires many more operations, higher skill, and more time per unit, contributing to a higher actual cost.

Many factories calculate labor using a concept like Standard Allowed Minutes (SAM), which estimates how many minutes it should take to produce one garment under normal conditions, thereby aiding in standard costing practices. Even if you do not calculate SAM yourself, you can ask the factory whether their quote is based on SAM and what assumptions they are using for efficiency. Cut and sew cost should include cutting, sewing, finishing, and line support. If a quote is very low, ask what is excluded, because low labor often turns into quality issues or delayed timelines.

Printing, Embroidery, and Branding Cost Allocation

Branding costs are underestimated because they include setup fees and per-unit fees. Printing cost depends on print type, number of colors, placement size, and quantity. Embroidery cost depends on stitch count, placement, and patch style.

A reliable way to calculate branding is to separate setup and per-unit charges:

Branding cost per unit = (Total setup fees ÷ order quantity) + per-unit print or embroidery cost + wastage allowance

Small orders feel expensive because setup fees are spread across fewer units. That is normal. You can reduce cost by simplifying placements, reducing colors, or batching multiple styles with the same branding method.

Washing, Dyeing, and Special Finishes

Washing and finishing can change cost and measurement stability. Many garments require enzyme wash, garment wash, silicone softener, brushing for fleece, heat setting, or special treatments. These processes add cost and may add shrinkage changes that impact final measurements.

If your product requires finishing, include it clearly as a separate line item in your cost sheet. Also confirm whether the factory quote includes finishing or if it is charged separately. For sustainable brands, finishing choices matter because some processes are more resource-heavy than others.

Packaging Cost Is Not Just a Polybag

Packaging includes more than a polybag. It may include tissue paper, hangers, size stickers, barcode stickers, carton labels, inserts, tape, and the carton itself. Packaging cost changes depending on whether you sell direct-to-consumer or wholesale.

A strong approach is to list every packaging component, cost it per unit, then allocate carton cost per piece. If you ship to fulfillment centers, packaging standards can be strict, and mistakes can create extra handling fees.

Quality, Testing, and Compliance Allowances

Many brands forget to cost for quality control and testing. If you sell internationally, lab testing may be required, especially for kidswear and performance wear. Even if it is not required, third-party inspections can protect your brand, especially for early orders with a new supplier. A practical method is to estimate expected total testing and inspection cost, then allocate per unit by dividing by order quantity. This is especially important for small orders, where the per-unit impact of indirect costs is larger.

Overhead and Contingency: Planning for Real Production Variance

Factories include overhead in pricing, but brands still need to plan for variance, including rework, minor defects, and small changes during bulk. A small contingency percentage can protect you from unexpected costs.

A typical range depends on garment complexity and supplier history. The goal is not to hide cost. The goal is to avoid false confidence from a cost sheet that ignores real-world variance. If your contingency is consistently high, it may be a sign that your tech pack, sample approvals, or supplier controls need improvement.

A Practical Cost Sheet Template You Can Reuse

A reusable cost sheet makes comparing suppliers much easier. You can build a template with consistent lines so every style is costed the same way.

Here is a simple structure you can copy into your spreadsheet:

Fabric, secondary fabrics, trims total, cut and sew, branding, washing and finishing, packaging, QC and testing, contingency, ex-factory total, then FOB and landed add-ons.

The key is that every cost line is visible. If something is not known yet, label it as estimated and update it after sampling.

FOB Cost: What to Include and How to Calculate It

FOB generally includes getting goods from the factory to the port with export handling. Depending on supplier, FOB may include cartons, inland transport, documentation, and forwarding charges.

If your quote is ex-factory, calculate FOB by adding export and forwarding costs and allocating per unit:

FOB cost per unit = Ex-factory cost per unit + (Total export and forwarding costs ÷ total units)

Always confirm what is included. A factory may quote FOB but exclude cartons. Another factory may include everything. You need visibility to compare properly.

Landed Cost: The Number That Protects Your Real Margin

Landed cost is what the garment truly costs when it arrives at your destination warehouse or fulfillment center. This is where many brands lose money because they price using ex-factory numbers only.

Landed cost includes freight, insurance, duties and taxes, customs clearance, and destination handling. Freight cost per unit depends on shipment method, total volume, and urgency. Air freight is fast but expensive. Sea freight is cheaper but requires earlier planning.

If your brand is not building landed cost into pricing, your margin is vulnerable.

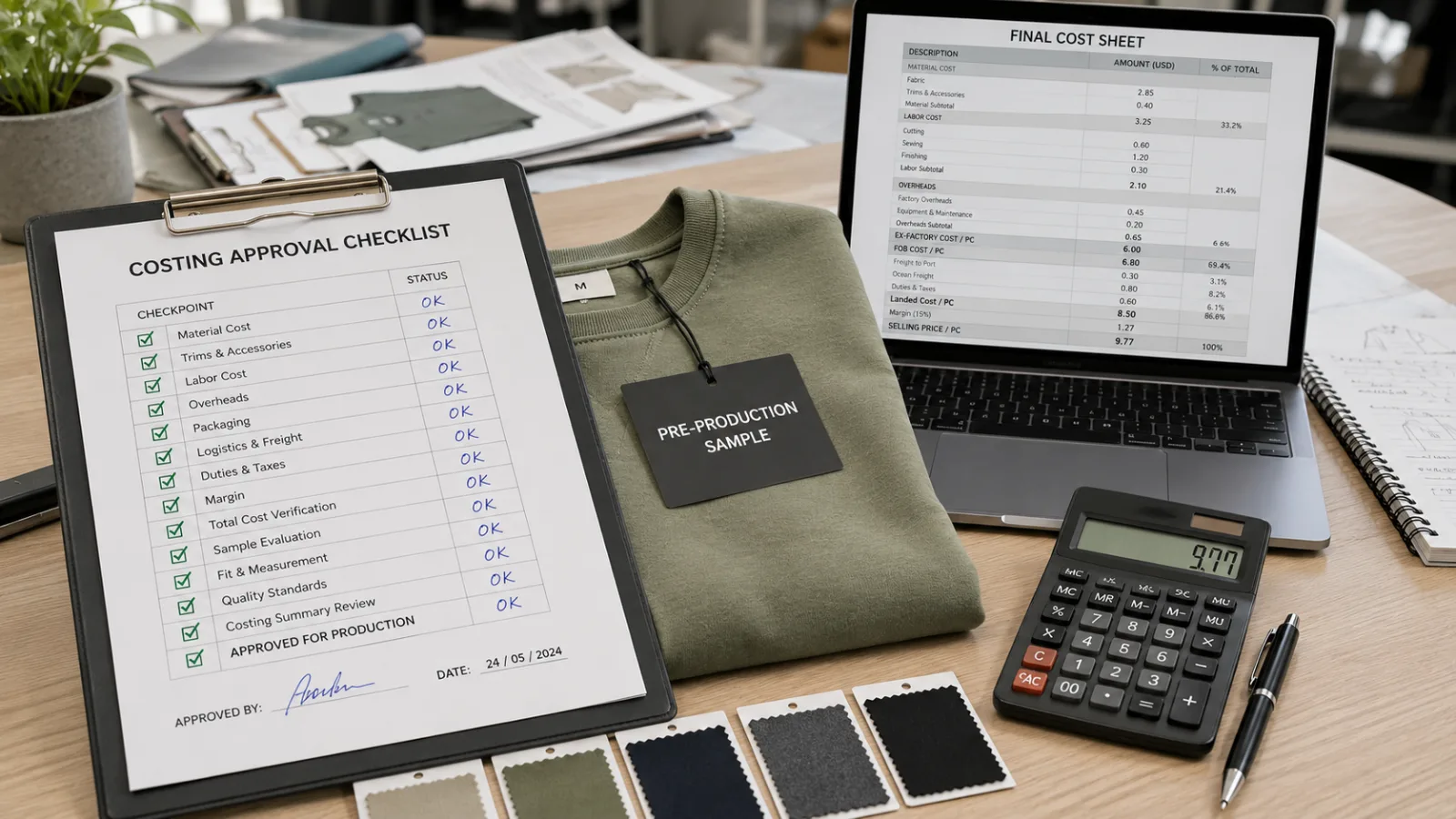

Margin Math: Turning Cost Into a Profitable Selling Price

Once you know landed cost, you can set pricing with real profit goals. Many brands confuse markup and margin. Margin is the percentage of the selling price that remains after cost.

A useful formula is:

Target selling price = Landed cost ÷ (1 - target gross margin)

If you plan to sell wholesale, you need a pricing ladder that supports both your margin and the retailer’s margin. That means retail price must be high enough to allow a wholesale price that still protects your profitability.

Accurate costing makes this decision straightforward instead of emotional.

A Worked Example: Costing a Premium T-Shirt

A worked example helps you see how all cost pieces fit together. Imagine a premium private label t-shirt with organic or high-quality cotton jersey, branded labels, and one small chest print.

Your fabric cost may be the largest part, but trims, print setup, packaging, and inspection can materially change unit cost. If the order is small, setup fees and label MOQ allocation may increase the unit cost more than expected. If the order is larger, those fixed costs spread out and unit cost improves.

The important lesson is that unit cost is not only materials. It is also how you allocate fixed costs across quantity, how you manage wastage, and how you plan shipping method to avoid emergency freight.

Costing for Sustainable Apparel: Planning the True Inputs

Sustainable fabrics sometimes cost more, and they may require extra documentation, traceability handling, and testing. Instead of avoiding these costs, the smarter approach is to include them clearly and communicate value through product positioning.

Sustainable costing becomes easier when your tech pack is detailed, because the factory can quote accurately on fabric, trims, and processes. Sustainable products also benefit from durability-driven construction, because better quality reduces returns and reduces waste.

When sustainability and costing work together, brands can maintain margin while offering better products.

Common Costing Mistakes That Destroy Profit Quietly

Many costing errors do not look like errors at first. They show up later as margin loss. The most common mistakes are ignoring wastage, forgetting label and packaging MOQs, not allocating print setup fees, underestimating freight and duties, and skipping QC and testing costs.

Another common mistake is costing before the product is stable. If your design changes after sampling, your cost sheet must be updated, too. Costing is a living document, just like your tech pack. Brands that win treat costing as part of product development, not as a last-minute spreadsheet.

How to Get the Best Pricing From Suppliers?

To get the best pricing from suppliers, start with thorough market research and clear specifications so quotes are comparable; knowing alternatives and benchmark prices strengthens your position. Build strong supplier relationships through regular communication and reliable forecasting, which often leads to preferential rates and early access to promotions.

Leverage competitive bidding and request bundled or volume discounts by consolidating purchases or committing to larger orders. Negotiate not only on unit price but also on payment terms, lead times, and bundled services to reduce total cost of ownership. Offer long-term contracts or staged commitments to secure lower pricing, and be prepared to walk away if terms don’t meet your targets. Finally, review performance and pricing periodically, using data-driven evaluations to renegotiate or re-solicit bids so your sourcing remains cost-effective over time.

How Tech Packs Improve Costing Accuracy

Tech packs improve costing because they remove assumptions. When your tech pack clearly defines fabric GSM, width, trims, stitch types, and finishing requirements, the factory can quote accurately and you can calculate consumption and processes with confidence. If your tech pack is vague, costing becomes vague. Then pricing changes after sampling, timelines shift, and margin planning breaks. Strong tech packs create stable costing, stable production, and stable reorders.

Garment Manufacturing Cost Advantages in Bangladesh

Bangladesh has become one of the largest apparel manufacturing hubs in the world and plays a critical role in the global fashion supply chain. The country exports over $45 billion worth of garments annually, supplying products to major international fashion brands and retailers. This strong manufacturing ecosystem has developed over decades and includes advanced production facilities, experienced garment workers, and an extensive textile supply chain.

One of the key advantages of manufacturing garments in Bangladesh is competitive production cost efficiency. Large-scale production capabilities allow factories to optimize labor productivity, material sourcing, and operational workflows through the application of activity-based costing. As a result, many global apparel brands choose Bangladesh for both basic and complex garment production.

In addition to cost advantages, Bangladesh offers skilled garment technicians and experienced production teams who specialize in various product categories such as knitwear, woven garments, activewear, and fashion apparel. The country also hosts a growing number of environmentally certified green garment factories, which support more sustainable production practices. Another important factor is scalability. Bangladesh’s garment industry is built to handle large production volumes while maintaining consistent quality standards. This makes it an attractive destination for clothing brands that need reliable production capacity as their collections grow.

Because of these advantages, many international brands work with apparel manufacturers in Bangladesh to balance cost efficiency, product quality, and scalable manufacturing solutions.

Apparel Manufacturing Partners and Costing Transparency

Many apparel brands work with manufacturing partners that support structured production systems, detailed tech packs, and transparent costing practices. Companies such as those utilizing advanced garment costing methods can significantly enhance their production efficiency. ApparGlobal support brands with product development, sampling, and scalable garment manufacturing workflows where accurate costing and clear specifications, including a detailed bill of materials, help improve production consistency. When manufacturers and brands align on materials, construction details, and quality standards early, costing becomes more predictable and production surprises reduce significantly.

A Simple Costing Checklist Before You Approve Bulk Production

Before confirming bulk, do a final costing check to ensure all components of the bill of materials are accounted for. Confirm fabric consumption and wastage assumptions, confirm trim pricing and MOQ allocation, confirm print or embroidery setup fees, confirm finishing costs, confirm packaging components, confirm QC plan, confirm what the quote includes (ex-factory or FOB), and confirm shipping method assumptions for landed cost. This checklist prevents the most common problem: approving bulk based on a cost sheet that is missing one or two major cost lines.

Apparel Manufacturing Partners for Accurate Cost Planning

Accurate garment costing often requires close collaboration between apparel brands and their manufacturing partners. Experienced manufacturers can help brands evaluate fabric consumption, trim requirements, production complexity, and operational costs before bulk production begins. This collaborative approach helps brands develop realistic cost sheets and avoid unexpected expenses during the production process.

Many clothing brands work with manufacturing partners that support structured product development, sampling, and transparent cost planning. Companies such as ApparGlobal assist apparel brands by providing garment manufacturing solutions where detailed tech packs, accurate cost analysis, and efficient production systems help ensure consistent quality and predictable production costs.

Working with experienced apparel manufacturers also helps brands improve communication across the supply chain. When factories clearly understand product specifications, material requirements, and construction details, they can estimate production costs more accurately and reduce the risk of costly revisions during sampling and bulk production. For growing fashion brands, partnering with a manufacturer that values clear technical documentation and structured costing methods can make garment production more efficient, scalable, and financially predictable.

ApparGlobal: Supporting Smarter Garment Costing and Pricing Decisions

Accurate garment costing requires more than adding fabric, trims, and sewing expenses. Apparel brands must also account for sampling, pattern development, fabric consumption, cutting waste, printing or embroidery, washing, packaging, quality control, freight, duties, minimum order quantities, and factory margins.

ApparGlobal helps fashion brands connect product design with realistic manufacturing costs before moving into bulk production. By reviewing material choices, garment construction, order volume, finishing requirements, and supplier capabilities, brands can identify where costs are increasing and where practical adjustments may protect quality without weakening the product.

Apparel businesses can explore:

- Sampling Program to test fabric, fit, construction, trims, and finishing before confirming bulk costs.

- Private Label Program to develop customized apparel using established product and manufacturing foundations.

- Manufacturing Support to coordinate costing, sourcing, production planning, and factory execution.

- Vendor Program to compare suitable material and manufacturing suppliers.

- Manufacturer Catalog to review production capabilities for different garment categories.

- Resources for further guidance on apparel costing, sourcing, sampling, and manufacturing.

A structured costing process helps brands avoid underpricing products, overlooking hidden expenses, or approving designs that cannot meet their target retail price. With clearer cost breakdowns and more reliable production planning, fashion businesses can set prices that support both customer value and sustainable profit margins.

Frequently Asked Questions About Garment Costing and Pricing

1. What is garment costing?

Garment costing is the process of calculating the total expense required to develop, manufacture, package, and prepare a garment for sale. It usually includes fabric, trims, labor, printing or embroidery, washing, finishing, packaging, overhead, quality control, freight, and other production-related expenses.

2. What is included in the cost of a garment?

A complete garment cost may include:

- Fabric and lining.

- Buttons, zippers, labels, elastic, and other trims.

- Cutting and sewing labor.

- Printing, embroidery, washing, or special finishes.

- Pattern development and sampling.

- Quality inspection.

- Packaging.

- Factory overhead.

- Testing and compliance.

- Freight, duties, and insurance.

- Waste and defect allowances.

The exact cost structure depends on the product, supplier, order quantity, and delivery terms.

3. Why is fabric usually the largest garment cost?

Fabric often represents the largest portion of garment cost because every unit requires a specific amount of textile material. Fabric price, width, weight, shrinkage, pattern direction, cutting waste, and minimum order quantity can all affect the final cost per garment. A lower-priced fabric may not always reduce costs if it has narrow width, high shrinkage, inconsistent quality, or excessive cutting waste.

4. How is fabric consumption calculated?

Fabric consumption is calculated by determining how much material is required to cut one garment. The calculation considers:

- Pattern dimensions.

- Garment size.

- Fabric width.

- Marker efficiency.

- Directional prints.

- Nap direction.

- Stripe or check matching.

- Shrinkage.

- Cutting waste.

- Size assortment.

Factories often create a marker to arrange pattern pieces efficiently and estimate the average fabric consumption per garment.

5. What is the CM cost in garment manufacturing?

CM usually means cut and make or cut and manufacture. It refers to the factory cost of cutting the fabric and sewing the garment.

Depending on the quotation, CM may also include basic finishing and factory overhead. It usually does not include fabric, trims, printing, washing, packaging, or transportation unless specifically stated.

6. What is CMT costing?

CMT stands for cut, make, and trim. Under a CMT arrangement, the buyer may supply the main materials, while the factory handles cutting, sewing, and selected trimming or finishing operations. Brands should confirm exactly which trims, services, and overhead costs are included because CMT definitions can vary between manufacturers.

7. What is the difference between the garment cost and the selling price?

Garment cost is the total expense required to produce and deliver the product. The selling price is the amount charged to a wholesaler, retailer, or final customer.

The selling price must usually cover:

- Product cost.

- Business overhead.

- Marketing.

- Storage.

- Payment-processing fees.

- Returns.

- Discounts.

- Taxes where relevant.

- Profit margin.

A garment that costs $10 to produce should not automatically be sold for $10. The business must include all expenses required to operate profitably.

8. How do you calculate the selling price of a garment?

A basic pricing formula is:

Selling Price = Total Product Cost ÷ (1 - Desired Profit Margin)

For example, if the total product cost is $20 and the desired gross margin is 60%:

$20 ÷ (1 - 0.60) = $50

This is only a starting point. The final price should also reflect customer expectations, competitor pricing, brand positioning, wholesale requirements, taxes, and promotional discounts.

9. What is the difference between markup and margin?

Markup is calculated based on the product cost, while margin is calculated based on the selling price.

For example, if a garment costs $20 and sells for $40:

- The markup is 100%.

- The gross margin is 50%.

Confusing markup with margin can cause brands to set prices that are lower than intended.

10. How does order quantity affect garment costing?

Larger order quantities can reduce the cost per garment because setup, sampling, printing, pattern development, and factory overhead are distributed across more units.

Higher quantities may also allow brands to negotiate better fabric, trim, and manufacturing prices. However, larger orders increase inventory costs and financial risk. Startups should balance unit-price savings with realistic sales demand.

11. Why do manufacturers have minimum order quantities?

Manufacturers and material suppliers set minimum order quantities because production requires setup time, machine allocation, labor planning, fabric dyeing, trim purchasing, and quality control. Very small orders may not cover these setup expenses efficiently. Some factories accept lower quantities but charge a higher price per garment.

12. How does garment complexity affect production cost?

More complex garments usually cost more because they require additional operations, specialist machinery, skilled labor, longer sewing time, and more quality checks.

Features that can increase cost include:

- Multiple fabric panels.

- Linings.

- Pockets.

- Custom hardware.

- Complex collars or cuffs.

- Pleats.

- Embroidery.

- Seam sealing.

- Special washes.

- Hand finishing.

- Difficult pattern matching.

Simplifying unnecessary details can reduce cost without significantly changing the product’s appearance.

Conclusion

Accurate garment production costing is a system, not a guess. When you calculate fabric consumption correctly, include realistic wastage, build a complete trims BOM, understand labor drivers, allocate branding and finishing costs, and then build up to FOB and landed cost, you protect your margin and make smarter manufacturing decisions. The best brands treat costing as part of product development and refine it as samples become more accurate. If you build a reusable cost sheet template and follow this method, you can price confidently, negotiate better, and scale production with fewer surprises.